")

Why 2025 is Different for Software Team Investments

For software professionals, the R&D tax credit is likely familiar. Accountants may have referenced it, or consultants may have approached you with overly optimistic savings projections. Historically, the R&D tax credit has occupied an ambiguous position: it is technically valuable, yet often confusing in practice and frequently overlooked until tax filing season.

2025 changes that.

This shift does not result from an increase in the credit itself. Rather, two important changes are compelling software teams to approach R&D credits as an operational process rather than a mere tax strategy:

- Modifications to the deduction of research costs and

- Heightened IRS documentation requirements

For founders, CTOs, and product leaders, the primary issue is not taxation, but rather the need for robust documentation and organizational discipline. In 2025, this distinction becomes particularly significant.

What Actually Changed for the 2025 R&D Tax Credit

Domestic R&D Costs Can Be Expensed Again

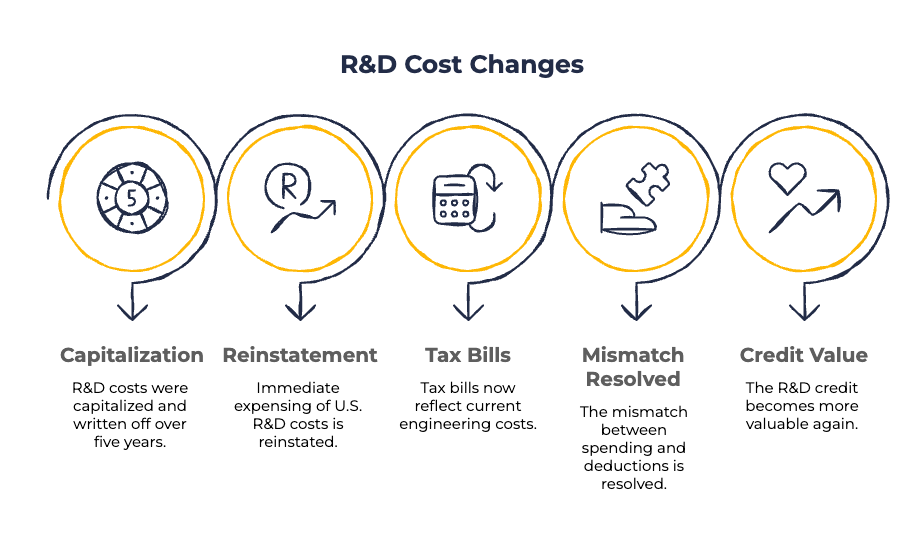

Between 2022 and 2024, something pretty painful happened to software companies. Research and experimental costs — the same engineering salaries you were paying every month — could no longer be deducted right away. Instead, they had to be capitalized and written off slowly over five years.

This change significantly disrupted cash flow for many software companies that were showing a cash loss, but had to show a profit on their taxes, which triggered tax liability.

Starting in 2025, that rule finally rolls back for U.S.‑based R&D. Domestic research costs can once again be deducted in full in the year they’re incurred. For software teams, that means:

- Your tax bill better reflects how much engineering actually costs right now

- The timing mismatch between spending and deductions largely disappears

- The R&D credit becomes meaningfully more valuable again

For organizations that capitalized R&D costs between 2022 and 2024, there may be opportunities to accelerate the deduction of remaining balances. Although the procedures are complex, the potential cash-flow benefits are substantial.

The IRS Is Getting Much More Specific About Documentation

The IRS quietly redesigned Form 6765, the form used to claim the R&D credit. The new version introduces a section that asks for detailed, component‑level information about what you built, what uncertainty you faced, and how you experimented your way to a solution.

For 2025, most companies technically don’t have to fill this part out yet. However, the intended direction of these changes is clear. Generalized statements such as “we developed new software features” are no longer sufficient. The IRS now requires:

- What specific system or feature were you building?

- What technical problem did you not know how to solve at the start?

- What alternatives did you test?

- Why the final approach won

Although an audit may not be imminent, the standards for documentation are being established.

Refund Claims Are Still a Minefield

If you plan to amend a return or file a refund claim for R&D credits, the rules are already strict. You must clearly identify:

- Each qualifying system or feature

- The research activities tied to it

- Who performed the work?

- The wages and costs tied to those activities

If these requirements are not met, the IRS has the authority to reject claims outright and frequently exercises that authority. Therefore, 2025 should be viewed as an opportunity to establish effective processes for future compliance, rather than focusing solely on retrospective claims.

👋 What kind of software work is your team currently doing?

Curotec helps software teams modernize legacy systems, rebuild core platforms, and scale complex applications.

Trusted by tech leaders at:

What the R&D Tax Credit Really Covers in Software

At a high level, the R&D credit rewards work where the technical outcome wasn’t obvious when you started. In software, that usually looks like:

- Designing a new platform or core service

- Re‑architecting a system to handle scale, reliability, or latency

- Building something that didn’t quite exist yet inside your stack

Eligibility does not depend on whether the outcome is considered “innovative” from a marketing perspective. Instead, qualification is determined by whether the team engaged in experimentation to achieve a functional solution. As a result, mature SaaS companies and internal platform teams may qualify for the credit to the same extent as startups.

How Software Work Qualifies Under the Rules

The tax code technically uses a four‑part test. In real life, it boils down to three questions:

- Were you trying to improve how something worked?

- Did you genuinely not know how to do it at the start?

- Did you test and discard multiple approaches along the way?

If all three criteria are met, the work typically qualifies for the R&D credit.

Internal‑Use Software Isn’t the Deal‑Breaker People Think

Many teams assume internal software never qualifies. This assumption is incorrect. Internal systems qualify all the time when:

- They support revenue or customer‑facing workflows

- They solve real performance or data constraints

- The technical solution wasn’t obvious

What doesn’t qualify?

Routine configuration. Cosmetic UI changes. Straightforward CRUD features your team could build in its sleep. The determining factor is not the software’s intended use. Rather, it is whether technical uncertainty was present.

Where Modern Engineering Work Fits

Agile methodologies, DevOps practices, and cloud-native delivery complicate documentation of R&D activities, but do not affect qualification for the credit. Examples that often qualify when uncertainty is real:

- Rebuilding a CI/CD pipeline to support zero‑downtime releases

- Refactoring a monolith to handle 10× traffic growth

- Designing a data pipeline that must hit strict latency targets

- Reducing cloud costs through architectural redesign

AI-assisted development activities may also qualify for the R&D credit. However, only the human decision-making component is considered eligible. Automated code completion is not eligible.

What Software R&D Costs Actually Count

Most software teams claim only one thing: wages. If engineers, QA, DevOps, or data engineers are directly working on qualifying problems, their time usually counts. The use of supplies is uncommon in software development. Contract development can count too—but only if you retain the rights to the work and can document what the vendor actually did.

Key R&D Tax Credit Changes for Software Teams

How Claims Are Going to Be Evaluated Going Forward

Even though the new Form 6765 detail section is optional in 2025, it’s basically a preview. The IRS wants claims organized around:

- Specific systems or features

- The uncertainty involved

- The experiments performed

- The people who did the work

That structure mirrors how good engineering teams already think. However, this information is often not formally documented. Yet.

A Real‑World Scenario

Imagine a SaaS company refactoring a monolith. The goal: support 5× more traffic without blowing up response times. The team doesn’t know upfront whether:

- Horizontal scaling will work

- A service split is required

- A new caching strategy will be enough

They test all three—two fail, one works. That’s R&D.

How to Claim the Credit Without Creating a Compliance Nightmare

Most teams don’t fail R&D claims because they weren’t eligible. They fail because they can’t prove what happened. The solution is straightforward. It may appear routine. Nevertheless, it is effective. Capture:

- Design docs

- Architecture decisions

- Jira tickets that show experimentation

- Pull requests tied to alternative approaches

This documentation should be maintained on an ongoing basis. Not in April.

The Mistakes That Are Going to Hurt in 2025

- Waiting until filing season to reconstruct narratives

- Grouping everything into one vague “platform project”

- Claiming routine work as R&D

- Treating documentation like an afterthought

Why This Matters More Than Ever

The 2025 R&D credit still puts real cash back into software companies. However, the credit now prioritizes organizational discipline over narrative explanations. Teams that build lightweight documentation into their delivery process will be fine. Teams that do not adopt these practices may encounter significant challenges in 2026.

Compliance Notice

This article is for informational purposes only and does not constitute tax, legal, or accounting advice. Tax rules are complex and subject to change. You should consult a qualified tax professional regarding your specific facts and circumstances before taking any action based on this information.

Curotec is not a CPA or tax advisory firm. Curotec is a software consulting company.

")